The last decade has not been kind to GoPro (GPRO -7.36%) shareholders. After reaching a market capitalization of over $10 billion shortly after its initial public offering (IPO), GoPro shares have fallen a whopping 97% from all-time highs, meaning that for every $100 invested at the stock price peak, only $3 remains today.

Yet, the company is still kicking. In fact, it generated $1 billion in revenue over the past 12 months. GoPro has gone from a technology favorite to a stock that has been tossed aside by most of the investing community. Does that make it a perfect opportunity for deep-value investors looking for bargain stocks to buy?

Stagnating subscriber growth, declining revenue

Before we get to the good, let’s set some expectations with GoPro. It is a struggling business, barely treading water for years. The company sells cameras for outdoor and extreme sports enthusiasts, allowing them to capture activities such as snowboarding, snorkeling, or mountain biking with high-quality video. Most of its sales come from these hardware devices and accessories associated with them.

After seeing a boom in demand in the latter parts of the COVID-19 pandemic, revenue has started to decline. Total revenue in the fourth quarter of 2023 was $295 million, down from $321 million in 2022 and $391 million in 2021. In order to spur demand, management has lowered product prices and gotten GoPro products into more retail locations. It is also spending more on sales and marketing.

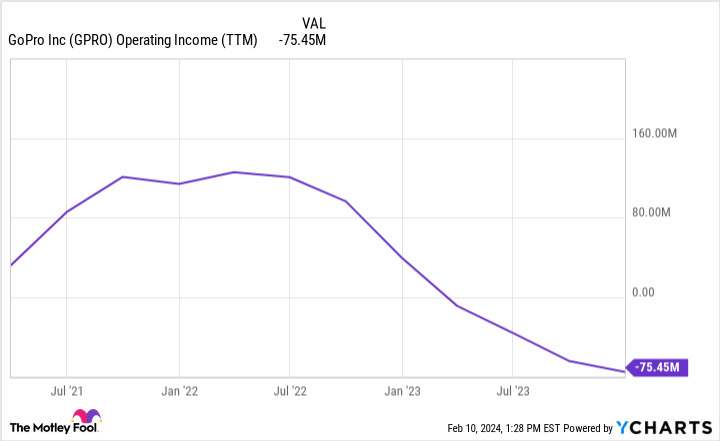

This has all had a negative impact on profitability, with the gross margin down to 34.4% in Q4 compared to 41.3% in 2021 and operating income falling to $2 million compared to $69 million in Q4 2021.

To diversify away from equipment sales, GoPro has made a push into add-on software subscriptions to smooth out its annual sales. Progress started great in this segment, going from 761,000 subscriptions at the end of 2020 to 2.25 million at the end of 2022. But then growth started to slow with subscribers only going from 2.5 million at the end of the third quarter to just a tad higher at 2.507 million by the end of 2023.

This is an issue, because GoPro’s subscription business is still much smaller than its hardware segment, generating under $25 million in quarterly revenue. Yes, this is high-margin revenue, but it is only around 10% of GoPro’s average quarterly hardware sales. Investors need to expect an acceleration in subscription revenue growth over the next few years if GoPro is going to get back to profitability.

Can an acquisition expand its customer base?

Despite these growth and profit struggles, GoPro management is not backing down from its expansion plans.

For example, it recently acquired Forcite Helmet Systems, a maker of technology-enabled motorcycle helmets. With an overlap in extreme sports customers, this acquisition makes sense, but will require sharp execution to integrate. Motorcycle helmets are outside of GoPro’s expertise (cameras), giving the company an entirely new market to address. For investors today, it adds yet another layer of uncertainty. But it also adds some upside potential.

No matter what GoPro’s growth strategy is, at the end of the day what investors care about is the bottom line. That will come from consistent revenue growth, gross margin expansion, and subscriber growth. Nothing else matters in regard to the stock price performance.

GPRO Operating Income (TTM) data by YCharts

Valuing the stock is tricky

Valuing GoPro stock is not simple, as the company’s profitability has gone through significant fluctuations. It has a market capitalization of $391 million and $153 million in net cash, which accounts for its outstanding debt. This brings its enterprise value down to a minuscule $238 million. That is barely more than twice its 2021 earnings of $113 million.

The problem is GoPro is now unprofitable, posting a $75 million operating loss in 2023. If you are thinking of buying the dip on GoPro stock, you need to be confident the company can return to the black over the next few years. This will come from growing software subscriptions, a better gross margin, and expanding its hardware sales. If the business continues to lose money, the stock likely has further to fall.

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.